How Insurance Claims Management Software Development Improves Accuracy by 60% and Speeds Up Claims by 40%

- Insurance claims management software is a must rather than just a mere option in environments where the volume of claims is high and the risk of fraud is significant.

- By automating manual workflows, minimizing errors, and speeding up decision-making, the software has a direct impact on operational efficiency.

- Companies that have integrated these systems saw a 60% improvement in claim accuracy and 40% faster processing times in real deployments.

- The McKinsey & Company report shows that automation reduces the time taken for claim processing by 50%, reducing operational delays and improving customer satisfaction.

- Automation, AI, and integrated workflows have extended beyond just being a mere tool. They are the need of the hour to be competitive.

- Insurers who adopt claim management software have achieved faster processing times and more accurate decisions. Also, they maintain cost control and scalability.

- On the other hand, those who still rely on outdated technology and manual processes risk more errors, slower settlements, and increasing customer dissatisfaction.

Insurance companies in the U.S. are sitting on a ticking problem. Claim volumes are rising, fraud is getting smarter, and the old way of doing things, like manual entry, phone follow-ups, and spreadsheets, simply isn’t keeping up. According to the Coalition Against Insurance Fraud, insurance fraud costs the U.S. economy $308.6 billion every year. That’s not a rounding error; that’s a systemic crisis.

And fraud is only part of the picture. A 2025 Experian Health report found that 65% of healthcare leaders say claims management has grown more complex since the pandemic. Denial rates are climbing. Reimbursements are slowing. Administrative teams are stretched thin trying to keep up.

This is exactly where insurance claims management software development comes in. The software handles the full cycle of an insurance claim, from the initial submission to the final payment, improving processes by removing the need for manual handling. Insurers who’ve deployed these systems are seeing up to 60% improvement in claims accuracy and 40% faster processing times. These aren’t projections. They’re being reported in real deployments.

Given these gains, the insurance claims management software development cost depends on the breadth of the system, but even mid-tier deployments pay for themselves rapidly when measured against fraud reduction, operational savings, and client retention.

What is Insurance Claims Management Software Development?

Insurance claims management software development is the process of building a digital system that manages the entire process of an insurance claim, from the moment it is submitted by a policyholder until the moment it is settled.

These systems automate a process that was very laborious and paper-driven. It does all the work, from data capture, document verification, routing, fraud checks, approvals, and communication, in one location, rather than adjusters navigating between their inboxes, spreadsheets, and PDF forms.

The software normally covers a wide variety of claim types, including health, car, property, and life insurance. Each of them is complex in its own way. For a vehicle claim, you may need images, telemetry data, and repair quotes. A health claim can contain an EOB, medical data, and prior authorization. A well-designed system brings all these elements together into a single, streamlined structure. For the best results, it’s important to hire an experienced insurance software development company.

The stakeholders include insurers, third-party administrators (TPAs), independent adjusters, and policyholders. Each group uses the platform differently, but they all get a speedier, more transparent experience when the system is running properly.

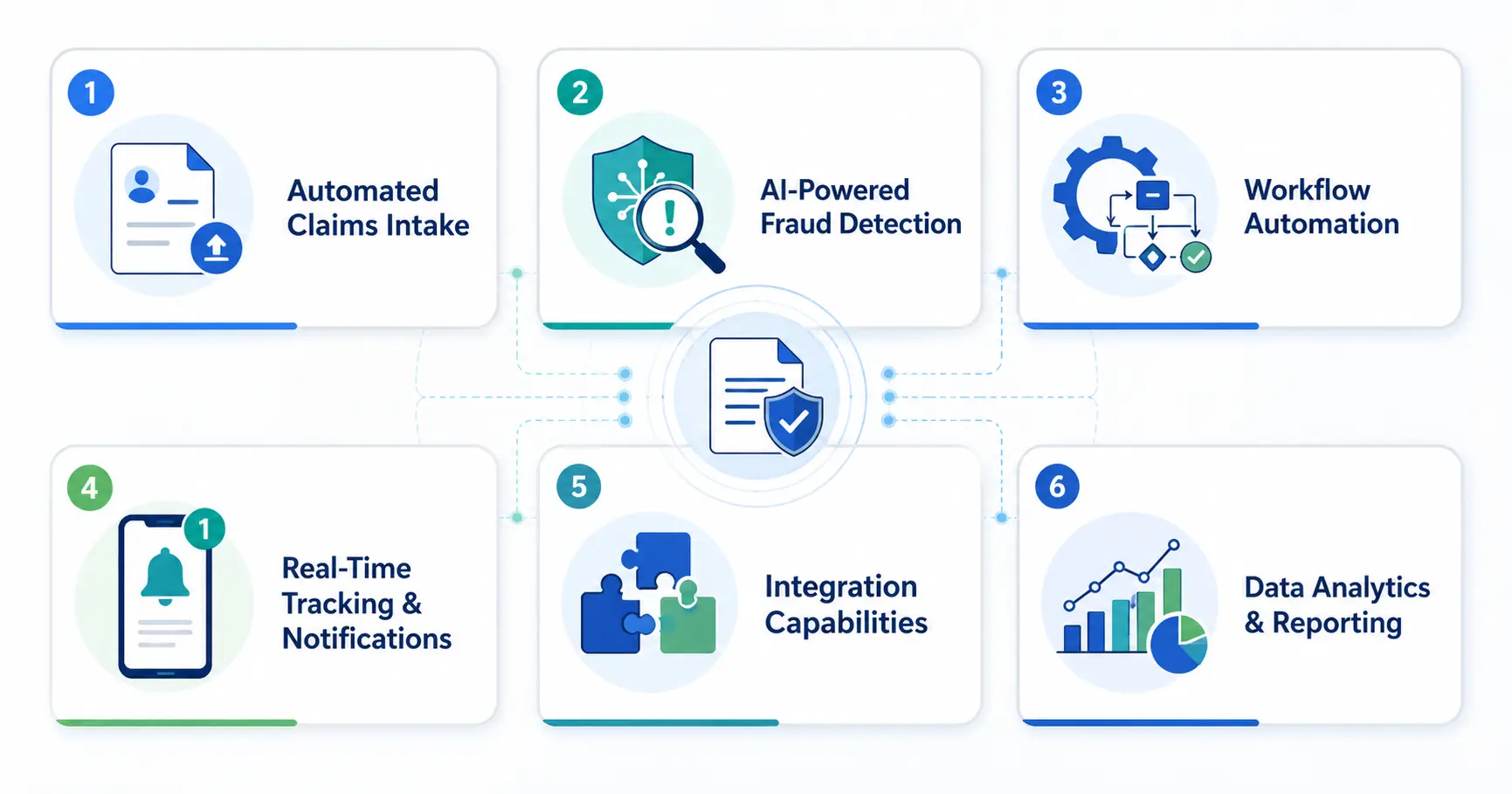

Key Features of Insurance Claims Management Software

Insurance claims management software combines automation, AI, integrations, and analytics to streamline the entire claims lifecycle, reduce manual effort, improve accuracy, and accelerate processing from submission to settlement.

Automated Claims Intake

When a claim comes in, the program digitizes it through web portals, mobile apps, email, or even API feeds from connected partners. OCR (Optical Character Recognition) and AI-based document capture read structured data from unstructured documents such as PDFs, pictures, and handwritten forms. This removes the first major bottleneck: manual data entry.

AI-Powered Fraud Detection

AI models compare new claims with past trends to spot anomalies that could escape a human eye. These include duplicate claims, mismatched medical bills, signatures that look faked for a staged accident, or claims sent at unusual intervals after a policy begins. AI can be a powerful tool for fraud detection, “with some platforms detecting 53% more fraud indicators than manual review.”

Streamline Your Claims Process with Smart Automation

Workflow Automation

Rule-based engines route claims to the right team based on type, complexity, value, and coverage rules automatically. No more manual triage. No more claims sitting in an inbox over the weekend. Complex claims go to senior adjusters; straightforward ones get fast-tracked for straight-through processing.

Real-Time Tracking & Notifications

Each stage is communicated to the policyholders. The system sends automated SMS or email notifications when a claim is received, when documents are needed, when an assessment is scheduled, and when payment is issued. This single feature alone dramatically cuts inbound call volumes to customer service teams.

Integration Capabilities

A good claims platform doesn’t exist in isolation. It integrates with CRM, ERP, and insurance administration systems, third-party data sources such as car history databases or weather APIs for property claims, and payment processors. For example, AXA Luxembourg saw a 3x speed in claims processing after deploying API-led integrations.

Data Analytics & Reporting

Dashboards provide insights into claim trends, cycle time, denial rate, adjuster performance, and fraud patterns, all through real-time data. Predictive analytics takes it one step further by looking at whether incoming claims are likely to be difficult or challenged, so managers may spend resources proactively rather than reactively.

How Insurance Claims Management Software Development Improves Accuracy by 60%

The accuracy problem in traditional claims processing isn’t about incompetent staff. It’s structural. When humans look at data from paper forms, errors happen. When adjusters work from memory and experience alone, inconsistencies creep in. Duplication happens when systems don’t communicate.

Automated software can do the following for each of these:

Removal of Errors From Manual Data Entry

Digital forms and OCR capture the data where it lives, with no middleman to transcribe it. In fact, according to the 2024 Experian analysis, 46% of claim denials are caused by missing or inaccurate data, a problem that is substantially solved with automated input.

AI/ML Verification

As data flows through the insurance system, AI models validate this information against policy definitions, coverage limits, past claims, and other external sources. If something doesn’t add up, it gets flagged before the claim gets through.

Standardized Processes

The same approach applies to all claims of a particular category. It doesn’t fluctuate depending on who is picking it up. Rule engines enforce consistency across thousands of claims simultaneously.

Fraud Detection Reduces False Claims

The FBI estimates P&C insurance fraud costs more than $40 billion annually. AI algorithms can see trends that manual reviews often overlook, catching incorrect rewards before they occur.

Automate Claims Processing and Improve Accuracy Instantly

No Duplication From Real-Time Syncing

With one data layer across all systems, the same claim can’t exist in many places with different information.

Before vs. After: A Real-World Example

Imagine a mid-size regional insurance company processing 5,000 auto claims a month through a manual process. Their team was working with a 22% mistake rate on claim data, mostly from manual entry and poor documentation management. After deploying a claims management platform with AI document capture and workflow automation, data errors were reduced to less than 3% in 6 months. Claim denials fell. Customer complaints followed. And the time their adjusters spent on rework dropped by nearly half.

How Insurance Claims Management Software Development Speeds Up Claims Processing by 40%

Speed in claims isn’t just about customer satisfaction, though that matters enormously. It’s a cost issue. Every day a claim sits open is a day someone is spending time managing it, following up on it, and waiting on it.

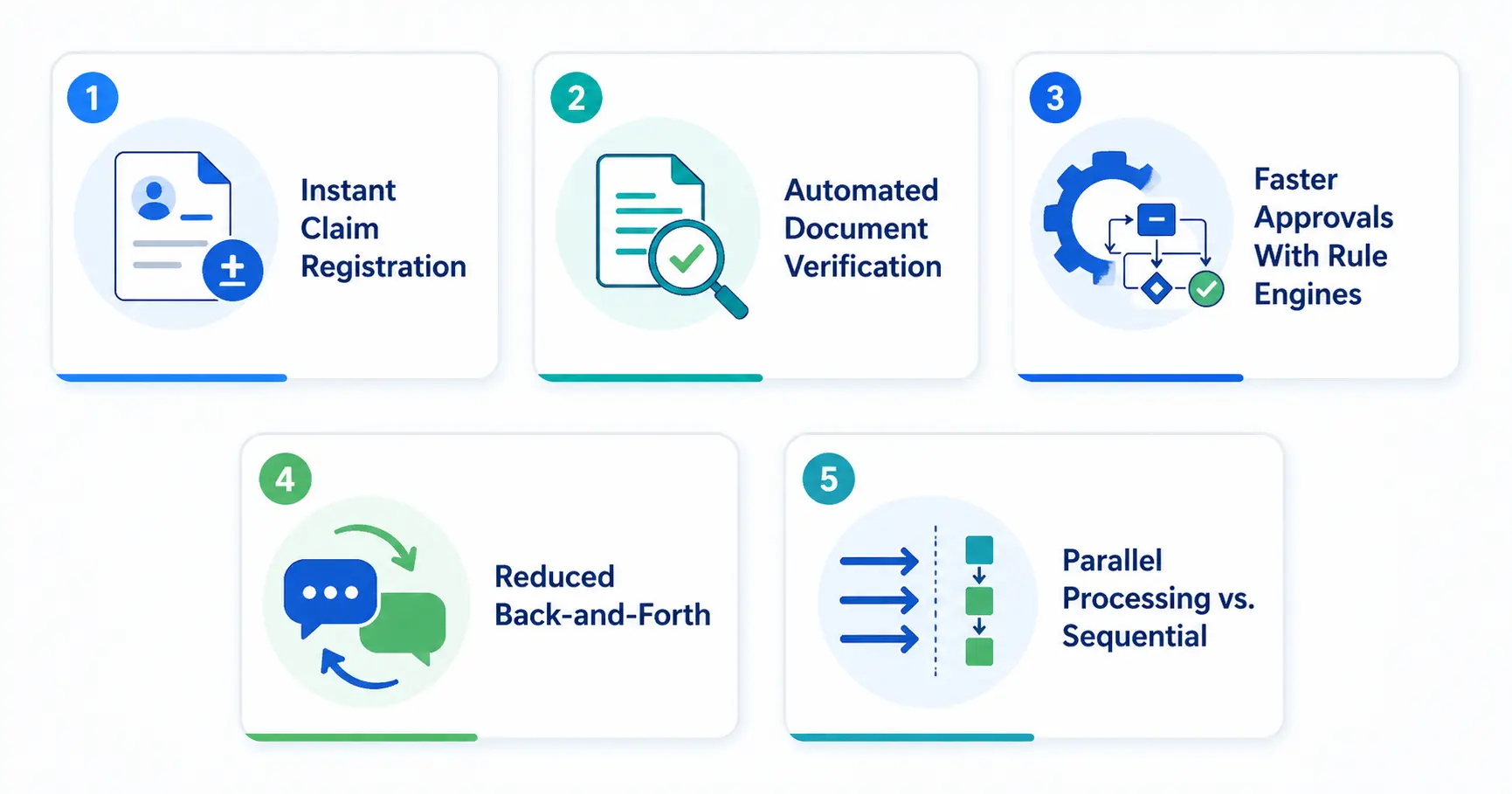

Instant Claim Registration

Digital intake means a claim that would have taken a day to log manually is registered in seconds. The policyholder submits, the system captures it, and a case is opened immediately.

Automated Document Verification

AI can examine and validate supporting papers, medical data, repair estimates, and police reports in minutes rather than days. According to McKinsey, automation can save claims processing time by as much as 50% over the whole lifespan.

Faster Approvals With Rule Engines

Simple, low-risk claims that meet all criteria can be approved and queued for payment without any human touching them. This is straight-through processing, and it’s already standard at leading insurers. Lemonade famously paid one claim in three seconds, an outlier, but one that shows what’s possible.

Reduced Back-and-Forth

The system proactively requests missing information during intake. By the time a human adjuster sees a claim, it’s complete. No more waiting for policyholders to send a missing form or for a repair shop to fax an estimate.

Parallel Processing vs. Sequential

In a manual setup, each step waits for the preceding step to complete. In parallel, numerous procedures are executed on a digital platform: a fraud check, a coverage check, and a document validation happen simultaneously.

Aviva’s use of AI in its motor claims department is interesting. They deployed 80 AI models that lowered liability assessment time for complex situations by 23 days, improving routing accuracy by 30% and saving more than £60 million ($82 million) in 2024 alone, according to McKinsey.

Build Faster, Smarter Claims Systems for Better Efficiency

Real-World Use Cases / Industry Examples

Real-world applications show how AI-driven claims systems improve speed, accuracy, and decision-making across health, motor, and property insurance workflows.

Automating Health Insurance Claims

AI-based claims platforms are allowing providers to handle clean claims in hours, not days. Automated eligibility checks, prior authorization flags, and EOB generation eliminate the back-and-forth that historically slowed health claims to a crawl. According to Experian Health, 45% of healthcare providers plan to invest in claims technology within six months, a number that reflects how critical this has become.

Motor Insurance Quick Settlement

Telematics data from connected vehicles can now trigger a claim automatically; the system detects an impact event, cross-references the policy, and initiates the intake process before the driver even calls in. Industry data show AI image processing analyzes provided photographs to assess damage with over 95% accuracy in severity estimation.

Property Insurance Damage Evaluation

After hurricanes or wildfires, the number of claims skyrockets overnight. Satellite imagery, drone camera footage, and imagery processing solutions powered by AI analyze property damage remotely and triage claims of varying severity based on damage sustained. This ultimately allows adjusters to be dispatched to areas where they are needed, which reduces the typical duration of property claims for catastrophic events by weeks.

Benefits of Insurance Claims Management Software Development for Insurance Companies

For insurance companies, investing in insurance claims management software development is a strategic decision that results in either operational efficiencies for the organization or may lay the groundwork to support the long-term viability of the company’s brand.

Decreased Operating Expenses

Automation eliminates repetitive data input and routing tasks, thereby decreasing the administrative overhead associated with processing claims for an insurer. The number of people working in traditional processes has been minimized by decreasing the number of employees performing traditional work.

Increased Customer Experience (CX)

An efficient claim experience is important in choosing an insurer, as well as being key from a competitive standpoint. A good experience increases customer satisfaction levels and retention compared to insurers providing traditional service experiences. It is judged based on what type of digital channel produces the best end-user experience.

Improved Compliance and Audit Readiness

Electronic records create an electronic audit trail of all activities associated with processing a claim, allowing insurers to maintain audit compliance in the eyes of regulators. This also helps to remain compliant with applicable data protection regulations without having to perform manual inspections.

Capacity to Handle Rapid Claims Increase

Software applications provide insurers with the ability to respond to unexpected increases in claims activity, whether they occur seasonally or due to a significant single incident. This guarantees that the system can take on more work without the need for the same level of employee requirements.

Benefits for Policyholders

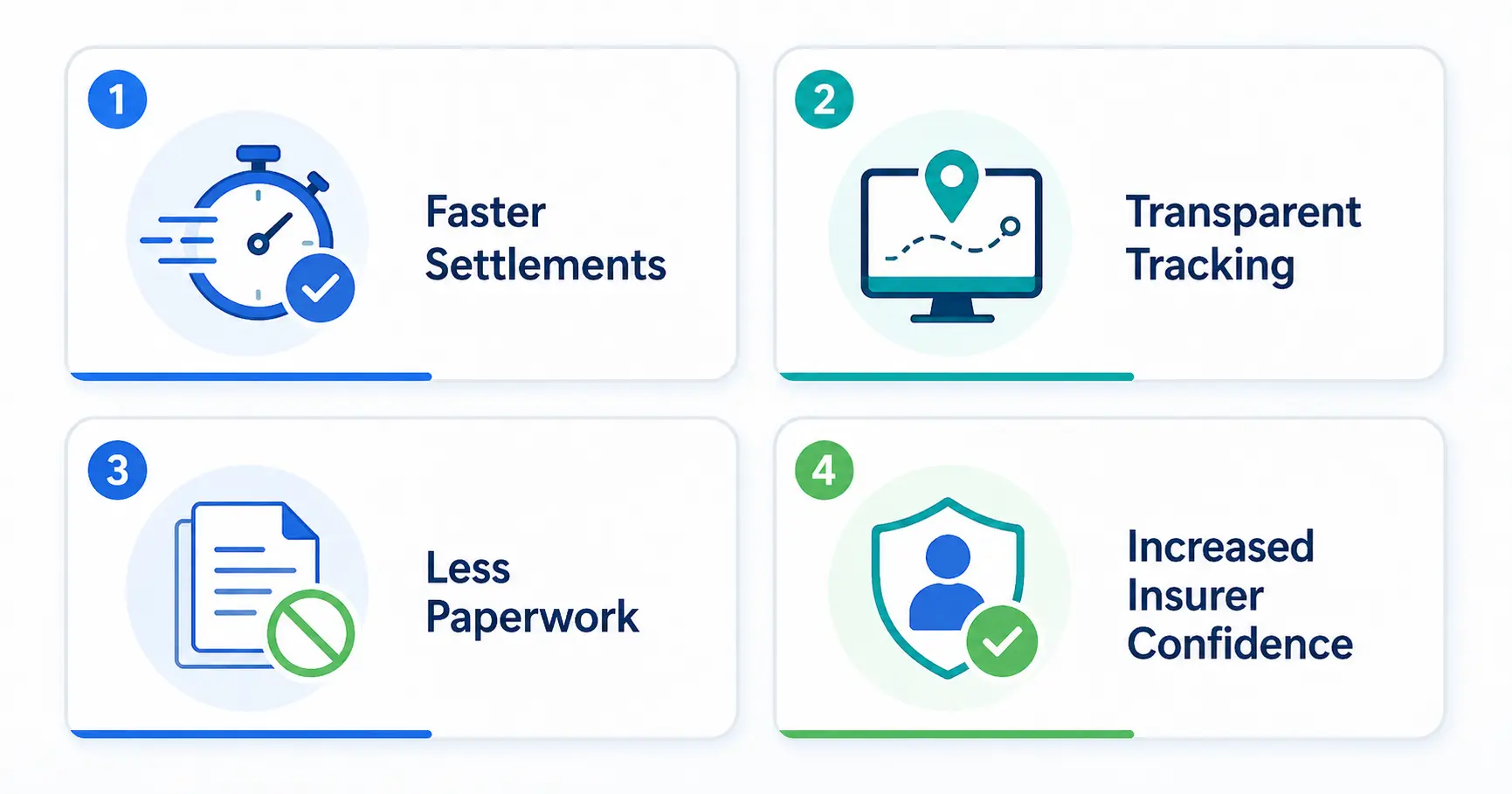

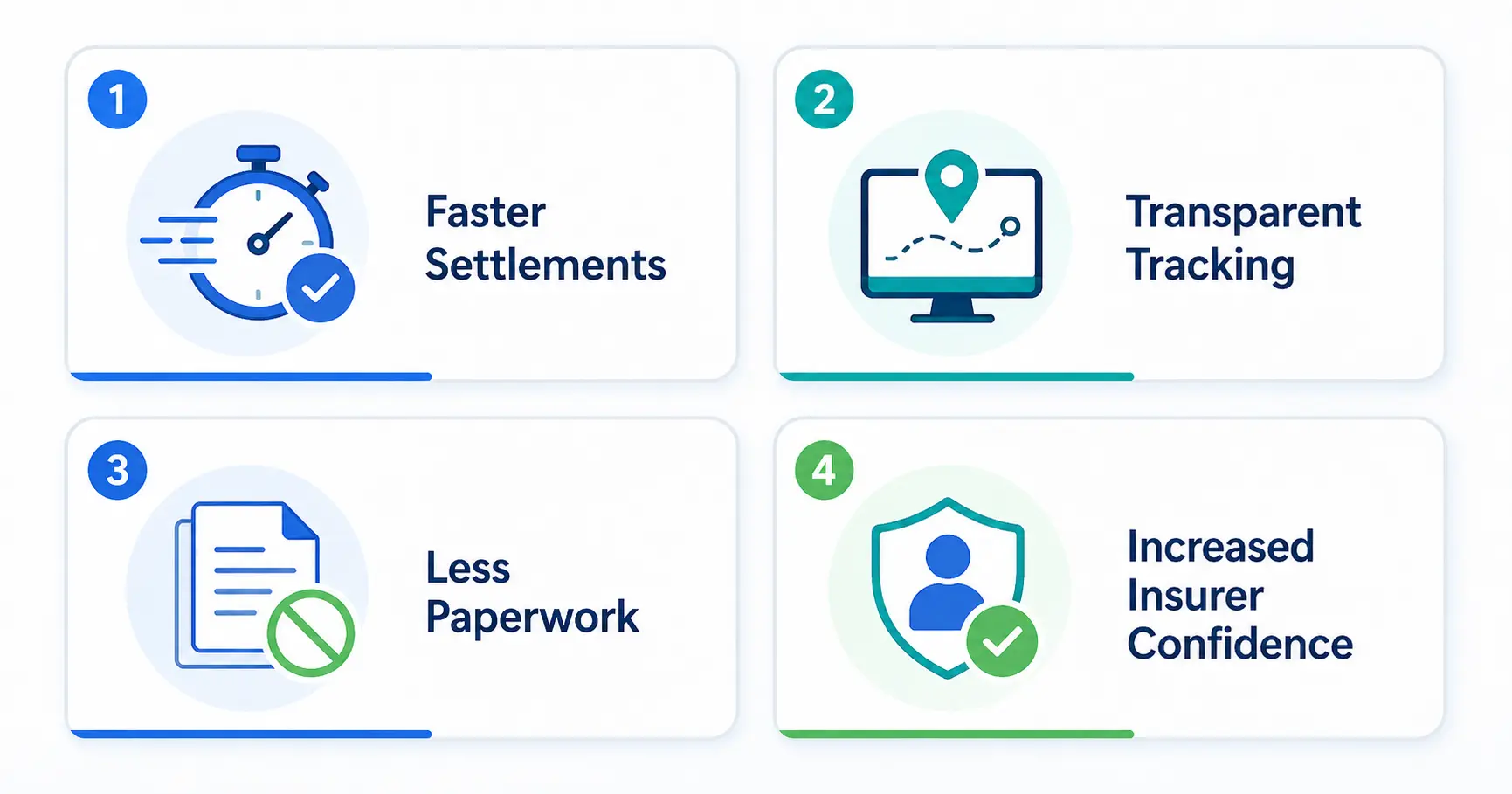

The move to modern insurance claims management software development profoundly changes the experience for the person at the heart of the claim.

Faster Settlements

Automated procedures remove manual handoffs, reducing the time from filing to payout dramatically. Policyholders regularly see claims that used to take weeks to settle get settled in minutes.

Transparent Tracking

The new systems have dedicated sites where the policyholders can check the status of their claims in real-time. Accurate visibility of the process eliminates any doubt about how it is progressing, either through interim steps or the final outcome of a claim.

Less Paperwork

Users can snap images or upload documents directly from their devices using mobile-based digital intake forms. This means no printing, physically signing, or shipping documents.

Increased Insurer Confidence

Continuous, reliable communication via a claim promotes long-term loyalty. When a company provides a clear and predictable process, it strengthens the professional relationship with the policyholder.

Minimize Delays and Maximize Accuracy in Claims Handling

Insurance Claims Management Software Development Cost

| Solution Type | Estimated Cost Range | Best For |

|---|---|---|

| Basic Solution | $20,000 – $50,000 | Small insurers, single line of business, limited automation |

| Mid-Level Solution | $50,000 – $120,000 | Regional insurers, multiple claim types, AI-lite features |

| Enterprise-Grade Solution | $120,000 – $400,000+ | Large carriers, full AI/ML, multi-system integrations, compliance modules |

These ranges align broadly with what the market reports. Enterprise-grade custom systems typically run between $100,000 and $400,000 depending on scope.

Factors Affecting Insurance Claims Management Software Development Cost

Complexity and Features

The more workflows you want to automate, the higher the insurance claims management software development cost. The scope includes straight-through processing and AI fraud detection.

AI/ML Integration

Custom model building and deployment take longer than rule-based automation. It adds expense. Worth it for fraud detection and damage assessment.

Third-Party Integrations

The more additional systems you need to connect to, such as CRM, ERP, payment gateways, and external data sources, the more development and testing time is added.

Compliance Requirements

HIPAA for health data, GDPR for international operations, and state insurance regulations; these all require specific technical controls that need to be built in from the start.

Development Team Location

U.S.-based development teams typically cost $150–$250/hour. Eastern European or South Asian offshore teams are $40–$100/hour with certain tradeoffs in communication and time zone overlap.

Insurance Claims Management Software Development Cost Optimization Tips

Begin with an MVP

Begin with the key workflows, such as intake, document capture, and basic routing, and test before layering on AI. This takes the risk out and gets you to value faster.

Use Cloud Infrastructure

Cloud-native implementations such as AWS, Azure, and GCP remove big infrastructure expenditures up front and allow you to scale pay-as-you-go.

Leverage Agile Development

It’s iterative sprints, so you can ship working things early, gather feedback, and adapt before you’ve blown the whole budget on a path that doesn’t suit you.

Future Trends in Claims Management Software

The technology here isn’t standing still. A few developments are worth watching:

AI-First Claims Processing

We’re moving from AI as a support tool to AI handling entire claim categories autonomously. Simple, low-value claims with clean documentation may require zero human involvement within a few years.

Blockchain for Fraud Prevention

Immutable ledgers make it possible to verify claim history across multiple insurers, like a direct counter to serial fraud. The blockchain insurance market was valued at $1.86 billion in 2024 and is on the rise.

IoT-Based Claim Triggers

Smart home sensors, telematics, and wearables can automatically detect insurable events and trigger claims. This removes the lag between an occurrence and notification and collects objective data that reduces conflicts.

Hyperautomation

Workflows can be optimized continually by combining AI, robotic process automation, machine learning, and process mining, not just one-time automation.

Let’s Build a Seamless Claims Management Platform Together

Challenges & How to Overcome Them

Implementing claims management software comes with challenges, but with the right strategy, insurers can overcome security, integration, cost, and adoption barriers effectively.

Concerns About Data Security

Claims data are sensitive health records, financial information, and personal identifiers. A good software ensures end-to-end encryption, role-based access control, and HIPAA and GDPR compliance. Security should be designed in from the start, not added later.

Integration with Legacy Systems

Most large insurers run on policy administration systems that are decades old. Modern platforms can connect via APIs and middleware, but this requires careful planning. It is best to start with read-only integrations before attempting write-back connections.

High Initial Development Cost

The MVP approach helps here. So does a phased rollout, like start with one line of business, prove the ROI, then expand.

Change Management

Adjusters who’ve worked a certain way for 15 years don’t automatically embrace new software. Training, internal champions, and early wins that demonstrate value are all part of a successful rollout.

How to Choose the Right Insurance Claims Management Software Development Company

Not every software firm understands insurance. The regulatory complexity, the claims workflows, and the compliance requirements aren’t intuitive for generalist developers. When choosing partners, check for:

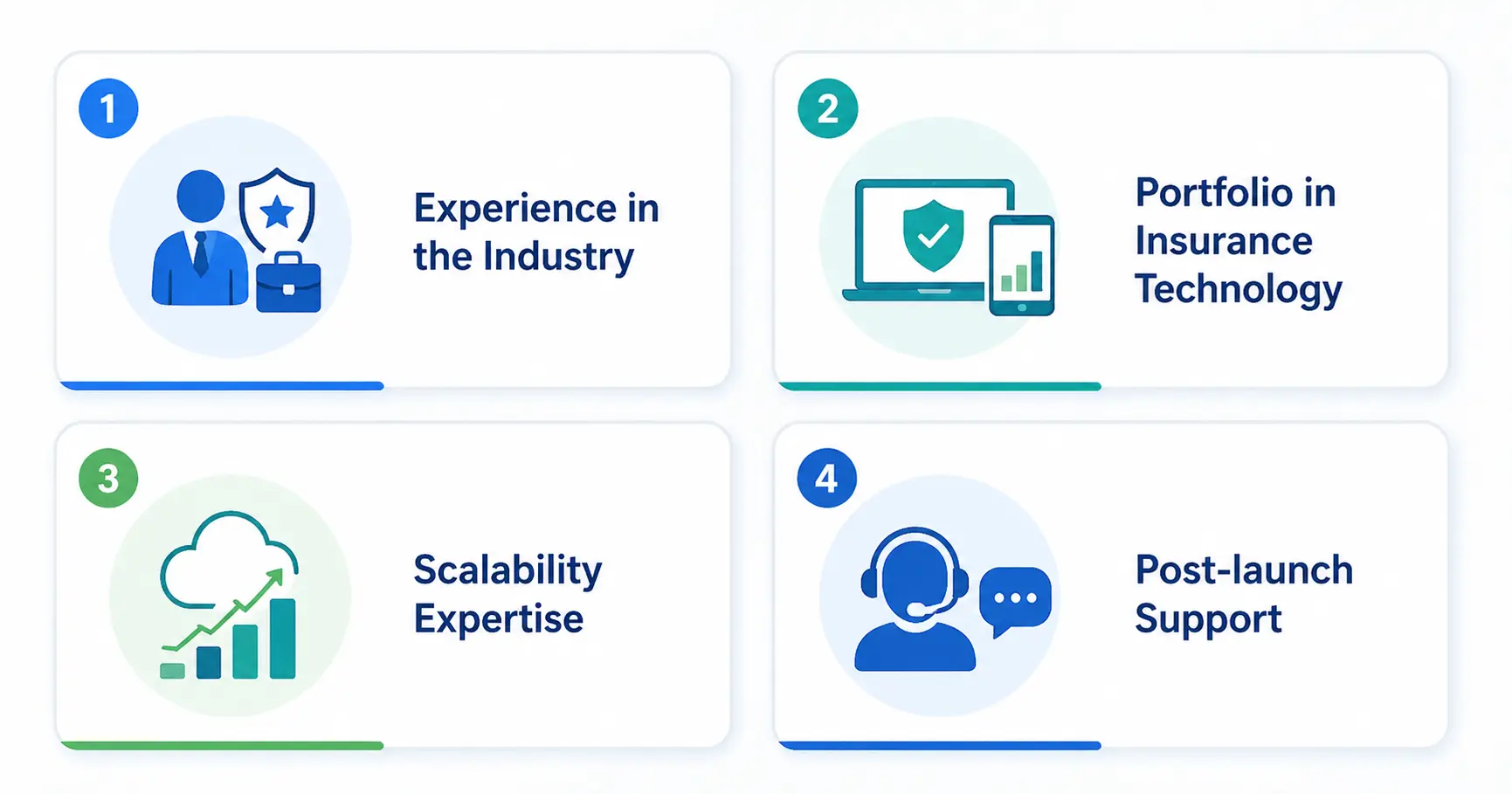

Experience in the Industry

Have they ever run claims systems before? Can they take you through how they addressed HIPAA compliance or multi-state regulatory requirements?

Portfolio in Insurance Technology

Ask for case studies. Real deployments with measurable outcomes are a better indicator than a capabilities deck.

Scalability Expertise

Your claim volumes won’t stay flat. The platform needs to handle growth, catastrophe spikes, and new lines of business without being rebuilt.

Post-Launch Support

Regulatory rules change. Fraud patterns evolve. AI models need to be retrained. You need a partner who stays engaged after go-live, not one who hands over code and disappears.

Within the insurance industry, The NineHertz has considerable experience in this area of technology with an extensive history of designing scalable, compliant systems for insurers’ health insurance, property insurance, and auto insurance claim processing. They provide complete support from architectural design through to post-launch optimization.

Conclusion

The figures paint a clear story. A 60% improvement in claims accuracy and 40% faster processing aren’t aspirational targets. These are the results insurers are already seeing with today’s claims management technologies.

Paper-based claims processing has served the industry for decades, but the volume of claims, the sophistication of fraud, and the expectations of digital-first clients have all outpaced what paper-based workflows can deliver. Insurance claims management software development is no longer just a technology improvement. It is a business requirement.

The alternative is to keep outdated processes and have competitors automate, resulting in delayed settlements, more exposure to fraud, more operational waste, and clients who will eventually move their business elsewhere.

Partner with professionals to design a claims system that is future-ready. The NineHertz has the insurance domain knowledge and engineering depth to build systems that not only work on day one but also scale and improve over time.

FAQs

1. What is insurance claims management software?

A claims management system is a digital solution that manages a claim from the time it is submitted until it is fully paid, verifying documents and information throughout the life of a claim. There is no longer a need for manual handling of paper documents, which makes submitting claims easier to process in a timely and accurate manner for insurance companies and policyholders alike.

2. How does claims software improve accuracy?

Automation helps reduce the amount of human error made due to the manual input of data into claims management systems. Utilizing AI, claims management systems can verify that information contained in claims is accurate while being processed, identify fraud opportunities early in the process, and assist in automating claims. These systems also provide a consistent reviewing process for all claims submitted and help create more accurate and timely claims processing.

3. What is the cost of insurance claims management software development?

The insurance claims management software development cost can vary greatly; a basic claims management system can cost between $20,000 and $50,000. More advanced claims management systems cost between $120,000 and $400,000 or higher depending on the complexity of development required. This depends on the development team, the features of the claims management system, any required integrations, and the regulatory standards to which the system must comply. Starting with an MVP system helps reduce the overall cost of your claims management system.

4. How long does it take to develop claims management software?

Typically, insurance claims management software development takes between 6 and 18 months depending on how complex the system is to build, as well as its integrations and compliance requirements. A very basic claims management system can be developed in approximately 3 to 4 months; however, an advanced system that utilizes AI technology will take longer since these systems require more extensive testing.

Great Together!

Latest Blogs

Insurance Mobile App Development & Cost: A Comprehensive Guide

Key Takeaways Insurance mobile apps are the digital interface designed for policyholders where they can track, manage, and file a…

Health Insurance Mobile App Development: Benefits, Features & Cost 2026

Key Takeaways With the end in sight of digital healthcare and InsurTech, insurers need to focus on developing mobile health…

Insurance Chatbots: Development, Examples, Use Cases in 2026

Key Takeaways Insurance chatbots are AI tools that help insurers automate workflows such as queries, claims, policy services, and sales.…